![Single Post [Template]](https://www.convergenceinc.com/wp-content/uploads/2019/09/sean-pollock-PhYq704ffdA-unsplash-1.png "Single Post [Template]")

Coverage of the Convergence Q3 update from ValueWalk – see original post

![]()

Convergence Inc. Announces Its Alternative Asset Management Industry Q3 Update

Alternative Asset Managers Convergence Insights Twelve Months Ended September 30, 2015

Q3 2015 Industry Headline-Alternatives Continue to Grow!

The number of alternative asset managers primarily advising private funds in our database grew 15% to 4,824 from 4,186. Manager growth was driven by new Managers coming into the market, including previously unregistered managers who registered, and existing registered Managers whose private fund assets under management exceed 50% of their total Regulatory Assets under Management.

The business complexity2 of the alternative asset manager industry in our universe on September 30, 2014 increased despite challenging and turbulent markets. The increase in business complexity was accompanied by material increases to staffing levels. The increase in non-investment headcount (middle-back office) is somewhat at odds with the trend toward outsourcing less core infrastructure. Perhaps Managers see many distinct choices and varying scope of services and technology solutions that make ‘Best Service Provider Fit” hard to discern.

Source of Convergence’s Insights

Convergence’s Q3 2015 insights are drawn from data we source from 16,000+ Form ADV and Brochure filings made by Registered Investment Advisors. ADV data from Advisors in business on 9/30/14 is our baseline and is updated during the year. In Q3 2015, 5,300 Advisors updated their Form ADV with 50% of this number is attributed to alternative asset managers. Our analytical approach allows us to follow alternative managers that have been in business for a full year and present an empirical view on how they are growing and changing.

Complexity drives work, cost and risk. Convergence tracks 31 Complexity Factors to develop various insights into how Managers manage capacity, infrastructure and meet new Regulatory and Investor requirements. With our Research, Analytics, Complexity, Benchmarking and Surveillance Tools, Managers, Service Providers and Institutional Investors can examine trends, peer and competitor intelligence empirically designed to build optimal infrastructure, select best fit vendors and enhance the overall Manager Due Diligence process.

Growth in our Universe of Alternative Managers

Convergence Insights

“The number of Alternative Asset Managers and assets will continue to grow as investors seek better returns and from asset classes less correlated with traditional equity and fixed income markets.”

Alternative Managers in our universe grew 15% to 4,824 and reported increases of 15% and 6%, respectively, in the amount of Regulatory and Private Fund Assets under Management3. The number of alternative private funds advised by Managers in business on September 30, 2014 grew 3% to 28,807.

Alternative Asset Managers also augmented the breadth of investment strategies and fund structures they advise, with 2.2% experiencing a re-classification by Convergence of their Primary Investment Strategy4 and 2.3% experiencing a re-classification of their Primary Fund Type 5 . Changes to a Manager’s primary investment strategy occur when they add new funds with strategies different than their legacy funds. Changes to a Manager’s primary fund type occur when the new funds they add are set-up in a different fund structure. For example, if a Manager launches a new debt fund in a closed-end private equity fund type whose total assets exceed the assets in their legacy debt funds that were set-up as hedge funds, their primary fund type would now be referred to as private equity while their strategy remained debt.

Leadership and Staffing

Convergence Insights

“Alternative Asset Managers cannot avoid hiring more middle and back office professionals to support increased business complexity and greater regulatory and investor requirements.”

Total headcount reported by Managers grew 11% to 80,728. This growth in staff reflects the growth in funds advised, the broadening of fund structures to capture new distribution channels and the management of increased business complexity. The number of Investment Professionals grew 9% to 39,889 representing 49% of alternative industry staff. This growth rate was outpaced by that of Non-Investment Professionals, which grew at a rate of 13% to 40,816, despite the fact that a large percentage of the middle and back-office operations are outsourced to third party service providers. Convergence believes complexity drives staff levels and that differences we see between complexity and headcount levels are based on the Manager’s culture and choice of service provider and their culture. Using an estimated all-in cost of 187.5k for a fulltime hire in the industry, we estimate that industry-wide personnel cost increased by 1.5bn per annum. All-in cost includes compensation and allocated overheads per person.

Q3 2015 represents the second consecutive quarter where the number of non-investment staff exceeded investment staff. This confirms Convergence’s view that non-investment hiring remains strong and is driven by complexity and regulation. Opportunities exist for Managers to work with Service Providers to efficiently manage growth by outsourcing the activities giving rise to non-investment hiring.

Business Complexity and Risk

Convergence Insights

“Complexity is here to stay-Managers must embrace and manage complexity to meet the return expectations of clients and limit operational and financial risks or lose business to alternative managers who have the scale to take on and manage additional complexity.”

Convergence’s alternative asset manager Complexity Index is a composite value of complexity factors that represents complexity and risk. The “Index” increased to 36.90, or 8%, from 34.21. The increase in complexity was driven by growth in affiliates, wrap fee programs, regulators, limited partners, total funds, private funds and public funds, and offset slightly by a decline in the Service Provider Index.

Industry Regulation

Convergence Insights

“60% or more of alternative asset managers in our universe may face significant financial liabilities because of unclear expense disclosures and practices, referred to by the SEC in recent actions as deceptive or misleading.”

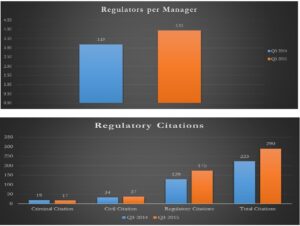

As expected, the regulatory environment continues to grow and intensify. The average number of regulators disclosed per Manager grew 23% to 3.93 versus 3.19. This increased level of regulation largely stems from new jurisdictions where business is being conducted and is consistent with the changes we see in fund types and strategies. Additionally, the number of regulators has a strong correlation to the number of regulatory citations disclosed by Managers. Regulatory Citations reported by our manager universe grew 30% from 230 to 290.

All alternative asset managers should pay close attention to the growing number of SEC actions taken against small and large alternative asset managers for “misleading or deceptive” expense allocations for the simple reason that 60% of alternative asset managers in our universe have similar expense disclosure challenges.

Service Providers

Convergence Insights

”Regardless of the high concentration of market share across the Top 10 in each Service Provider Segment, there are simply too many firms servicing Managers which robs each of the financial scale needed to reduce systemic costs and reinvest in their business. Universal Banks will continue to shed businesses that do not generate enterprise value and/or cover increasing capital requirements-Convergence sees movement suggesting some big deals are in the making and sees smaller more nimble Service Providers gaining momentum!”

The Convergence Service Provider Index, defined as the sum of service providers used by Managers increased 1.2% to 7.95 driven by increases to